The term dollar-cost averaging (DCA) refers to the practice of constantly committing a set amount of money on a scheduled basis (such as every week, month, or every quarter) to invest in securities , regardless of the current market price of these securities. The US Securities and Exchange Commission (SEC) has explained how using a DCA strategy can help you with the management of risk through a repetitive approach of increasing your investment by using the same amount of money over an extended period of time.

Three things to understand immediately: DCA automatically makes you buy more shares when prices are low and fewer shares when prices are high, which reduces your average cost per share over time. It removes the need to predict market movements, which even professional investors consistently fail to do accurately. And it turns investing into a system rather than a decision, removing the emotional component that causes most retail investors to buy high and sell low.

DCA is particularly powerful for Saudi investors building US stock positions because it allows you to invest consistently during market volatility without the anxiety of trying to time entry points. Whether you are building a position in S&P 500 index funds, halal ETFs, or individual tech stocks, the discipline of regular investing consistently beats the anxiety of waiting for the "right moment."

How Dollar-Cost Averaging Actually Works

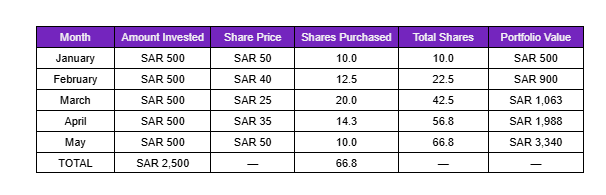

The mechanics are simple. You decide on a fixed amount to invest and a regular schedule. You invest that amount on that schedule, no matter what the market is doing. Here is a concrete example using Saudi Riyals:

Total invested: SAR 2,500. Total shares acquired: 66.8. Average cost per share: SAR 37.42 (SAR 2,500 ÷ 66.8). Average market price over the period: SAR 40. Your average cost (SAR 37.42) is lower than the simple average price (SAR 40). This is the DCA effect at work.

Why did DCA produce a lower average cost? In March, when the price dropped to SAR 25, your fixed SAR 500 bought 20 shares, your best month by far. Because DCA kept you investing through the dip rather than panicking and stopping, you accumulated more shares at the lowest price. Investors who tried to "time the market" and stopped contributing when prices fell in February and March missed these critical accumulation months.

Start your own DCA plan on Raseed from just SAR 1 ($1) invest in US stocks, halal ETFs, or Saudi stocks on any schedule you choose. No minimum. No hidden fees. Set up your first DCA investment on Raseed →

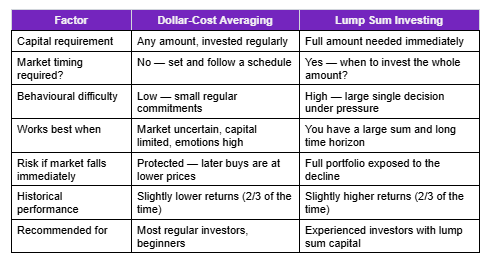

DCA vs Lump Sum Investing — Which Produces Better Returns?

Dollar-cost averaging (DCA) is the practice of investing a fixed amount of money at regular intervals (such as every week, every month, or every quarter) into selected securities, regardless of the current market price of these securities. The US Securities and Exchange Commission (SEC) has explained how using a DCA strategy can help you with the management of risk through a repetitive approach of increasing your investment by using the same amount of money over an extended period of time.

Lump sum investing has two things that most people don't have: significant amounts of money to invest in one time and the patience to see that entire investment drop in value the first time the stock market goes lower than it does today.

DCA's real advantage is behavioural, not mathematical. The SEC's own guidance confirms that "trying to time the market, waiting for the best time to buy or sell an investment is typically impossible even for professional investors." DCA solves the timing problem by eliminating it entirely. You do not try to time the market. You invest on schedule.

DCA for Saudi Investors — Specific Considerations

SAR-denominated DCA on US stocks. When you invest in US stocks from Saudi Arabia, your transactions happen in USD but your income is likely in SAR. The USD/SAR exchange rate is pegged at approximately 3.75 SAR per USD and has been stable for decades, which removes currency risk from the DCA equation for Saudi investors. You simply convert SAR to USD at the time of each investment. This is a significant advantage compared to GCC investors from countries with floating currencies.

Monthly salary alignment. Most Saudi professionals receive monthly salaries. A monthly DCA schedule aligns perfectly with pay cycles, you invest a fixed percentage of your salary each month automatically. The behavioural benefit is substantial: automating the investment removes the active decision each month, which is where most investors stumble.

Starting small is completely valid. You do not need SAR 5,000 or SAR 10,000 to start DCA. Our guide on how to invest SAR 1,000 in US stocks shows how beginners can start building a real portfolio with fractional shares. The power of DCA is in the consistency, not the amount. SAR 500 per month invested consistently for 10 years at average market returns builds far more wealth than SAR 5,000 invested once and forgotten.

DCA and the TASI market hours. Because TASI operates Sunday through Thursday, a monthly DCA plan for Saudi stocks should specify the exact day of the month, for example, the first Sunday of each month. Ensure your chosen date is not a Saudi national holiday or Eid. For US stocks, monthly DCA can target any market day, but avoid scheduling on known US holidays. See the complete Saudi and US market hours guide for holiday calendars.

Step-by-Step: How to Set Up a DCA Plan on Raseed

Decide your monthly investment amount. Choose an amount you can sustain through any market condition, not the maximum you can invest in a good month, but the amount you could maintain even in a difficult month. Financial advisors commonly suggest starting with 10–20% of monthly income for investing.

Choose your target assets. Decide whether you are DCA-ing into individual US stocks, ETFs, halal-screened funds, or TASI stocks. For beginners, broad market ETFs or index funds are typically the DCA-friendly starting point because they require no stock-picking decisions. Our guide on index fund investing covers how to choose.

Pick your schedule. Monthly DCA aligns with salary cycles for most investors. Weekly DCA produces slightly more averaging (more purchase points) but requires more frequent attention. Set a specific date for example, the 5th of every month and stick to it regardless of market conditions.

Automate if possible. Remove the active decision from each investment cycle. When a monthly payment requires you to actively log in, research prices, and decide to buy, there will be months you skip. Automation eliminates this friction.

Ignore short-term noise. The DCA discipline breaks down the moment you start saying "I'll skip this month because the market looks bad" or "I'll invest double this month because prices look good." Either decision defeats the purpose. The plan only works if you follow it consistently through all market conditions.

Review annually, not monthly. DCA performance should be assessed over years, not months. An annual review of your average cost versus current prices, total shares accumulated, and alignment with your financial goals is appropriate. Reviewing weekly or monthly leads to unnecessary tinkering.

Invest through fractional shares from $1. Trades capped at $3. No maintenance fees. Open your Raseed account and start your DCA plan today →

DCA and Compound Interest — The Combination That Builds Wealth

DCA alone is a powerful strategy. DCA combined with compound interest is how ordinary investors build extraordinary wealth over time. Compound interest means that the returns you earn in one period generate their own returns in the next period. The longer you stay invested, the more aggressively compounding works in your favour.

Example: If someone invests SAR 1,000 every month into a mixture of investments for 20 years, that person can expect to have around SAR 589,000 at the end of that period. Even though that investor only put in SAR 240,000 during the 20 years, about SAR 349,000 of the total will be due to compound interest. On average, for every SAR 1,000 invested each month over 20 years, the investor will receive back about 2.5 times the original amount of their investment.

One of the reasons to start investing as soon as possible...even with a small amount...is to produce better results than waiting until you have enough money for a large investment. The DRIP (dividend reinvestment plan) guide will explain how reinvesting dividends grows compounding even further, creating a cycle in which returns generate additional returns over time.

3 DCA Mistakes Saudi Investors Must Avoid

Mistake 1 — Stopping during market downturns. This is the most common and most costly DCA mistake. Bear markets and market corrections, when prices have fallen, are precisely when DCA is most powerful. Every SAR you invest during a downturn buys more shares at lower prices, setting up exceptional future returns when the market recovers. Stopping DCA when markets fall means missing the best accumulation opportunity of the cycle.

Mistake 2 — Investing in a declining asset and calling it DCA. DCA works as a strategy when the underlying asset has genuine long-term value, a broad market ETF, a quality stock with strong fundamentals, or a diversified halal fund. It is not a strategy for a failing company or a speculative cryptocurrency with no underlying value. "Averaging down" into a company that is genuinely deteriorating just increases losses at lower prices.

Mistake 3 — Setting an amount too large to sustain. Some investors set an overly ambitious DCA amount in an enthusiastic moment and then cannot maintain it during difficult months. A DCA plan at SAR 300 per month that you sustain for 10 years is worth far more than a SAR 1,000 plan that you abandon after 6 months. Sustainability beats ambition in long-term investing.

Frequently Asked Questions

What is the best frequency for DCA — weekly, monthly, or quarterly?

Monthly DCA aligns with most Saudi professionals' salary cycles and is the most practical frequency. Weekly DCA provides slightly more price averaging points but requires more engagement. Quarterly DCA reduces the number of purchase opportunities. For most investors, monthly is the best balance of simplicity and effectiveness.

Can I use DCA for TASI stocks from Saudi Arabia?

Yes. DCA works on any publicly traded security TASI stocks, US stocks, ETFs, or index funds. For TASI, simply choose a fixed amount in SAR and invest on the same day each month (or week). Saudi Aramco, Al Rajhi Bank, and SABIC are commonly used for Saudi-focused DCA portfolios.

Is DCA better than trying to time the market?

According to Charles Schwab's research, "trying to time the market, waiting for the best time to buy or sell an investment is typically impossible even for professional investors." DCA does not attempt to time the market, it removes timing from the equation. This makes it structurally superior to market timing for the vast majority of retail investors.

How much should I invest each month using DCA?

It’s generally advised to contribute 10% to 20% of your monthly income. However, determining how much to contribute is highly individual based on your financial status, level of savings, overall monthly expenses, and investment objectives. The biggest factor in selecting your contribution level is consistency; if you can commit to making a monthly contribution regardless of whether the economy is doing well or if you’re experiencing personal financial hardships, this is the best option for you.

Does DCA work for halal investing?

Yes. DCA is a strategy for how you invest, not what you invest in. It works equally well for halal ETFs, Shariah-compliant stocks, and other Islamic finance-compatible instruments. The consistency and discipline of the strategy align well with Islamic financial principles of measured, sustainable wealth building.

DCA works for US stocks, Saudi stocks, and halal ETFs — all available on Raseed from one DFSA-regulated account. Start your DCA journey on Raseed — it's free to open →

Related Articles on Raseed Learn

Compound Interest Explained for Saudi Investors | How to Invest SAR 1,000 in US Stocks | Index Fund Investing in Saudi Arabia

Best Halal ETFs for Saudi Investors 2026 | 5 Steps to Diversify Your Portfolio | Dividend Reinvestment (DRIP) Guide